We are going to start this course off by talking about time. One of the most common questions I always get asked by beginners is ‘how much time does it take to master the charts?’

As a trader who has over seven years of experience, what am I suppose to say when someone asks me that question? Mastering the charts comes down to so many difference factors and beginners need to understand this. I have had many one on one webinars over the years with traders, and the majority of them suffer from emotional trading. You could be an absolute wizard on the charts, but if you are going to trade with emotions then you are going to find yourself in a endless circle of blowing accounts.

The real question should be… How many blown accounts will it take you to stop trading with emotions, and learn to master the charts?

The real difference between an experienced trader and a beginner is not the about of training videos they have watched, but the amount of time they have spent on the charts. Unfortunately in trading, its something you can not skip. You can spend thousands on the latest training or indicators, but none of that is going to help you, unless you put the time in on the charts. This is why we start this course off by talking about time. What makes me stand out above the rest of the traders when it comes to Support & Resistance is the amount of time I have spent learning it, and trading it. It sounds like an odd comparison but look at trading like playing a video game. If you play 10 video games at once you will be good at it. However if you play one video game, every day for the next two years, you can almost guarantee you will be the best in the world at it.

This is the same with trading. If you spend the next two years going from strategy to strategy, price action to price action, You will be average at it. However if you all you focused on was Support & Resistance, you will be an expert at it. This is why I stand out above the rest when it comes to mastering this skill, and its the reason why you are here today reading this.

In my first year of trading, I learnt absolutely nothing apart from installing strategies and watching videos. Imagine the frustration I was in after spending thousands of pounds and I had learnt nothing. I kept going back a fourth with Support & Resistance over the next couple of years, and in the end I came to the confusion that I needed to master it. Every strategy I had learnt, I noticed Support & Resistance had a roll to play in making that strategy profitable. Even learning a more advanced level of Price action that institutions traded, I noticed Support & Resistance played a part in that. For example if you trade liquidity and order flows, where is liquidity most likely to be in the market?

That is right…. Above or below Support & Resistance levels. So if I wanted to learn and trade liquidity, I needed to learn Support & Resistance first to know where liquidity is going to be sitting.

This is why I made it my mission to learn the art of Support & Resistance Trading.

I have been profitable for around six years now (2023), and I have not followed another trader during that time. This is not because I have been busy, its because I did not want the distractions from other traders. What has made me s0 successful at trading, is the amount of time I have spent on the charts. Everything I have learnt about Support & Resistance has come from my time watching the charts. This is why I can assure you, you have not seen any of this training before. Everything I show you in this course has come from my own experience on how the charts move, and this is why we start this course off talking about time.

When it comes to trading, you can never set a time on how long it will take you to become successful at trading. In fact if you put pressure on your own trading with setting goals and time restrictions, you will only end up frustrated. This is why you want to relax and enjoy your trading. The more you enjoy trading the more you will get out of it and the more you will want to carry on learning.

A time management routine is a crucial element to your success. Without having a strict daily plan, it is easy to waste precious hours every day fumbling around looking for something to do, procrastinating, or worse – watching TV. Did you know that if you watch TV for only 1 hour a day, you will spend more than 2 and a half years of your life on the couch. Considering the average person is only awake for around 53 years, this equates to roughly 5% of your waking days. When you turn 80 and look back over your life, do you think the time you spent watching TV will have improved your experience on earth, helped you achieve your goals or helped you make a difference in the world? Many people complain about not having enough time, when in fact they have just as many hours per day that were given to Helen Keller, Michaelangelo, Mother Teresa, Leonardo da Vinci, Bill Gates and Albert Einstein. 9 times out of 10 it’s not the amount of time, but the use of time that’s the issue. A well oiled time management routine allows you to make the most of each day, increases productivity and launches you towards success. If you still have a day job, then a lot of your time is already accounted for, so learning this skill is even more important to you as you have limited time to be productive.

“You make a living from what you do 9 til 5 but you make a fortune from what you do 5 til 9″

Time management principles all boil down to 3 simple points that will literally add years of productivity to your life.

Plan

A daily plan should be written up each morning or even the night before. As with goal setting, writing out your plan helps you stay on track and remain focussed on your tasks. Complete the tasks you least wish to do first, this way you can get them out of the way early in the day when you still have plenty of energy. Besides your primary to do list, don’t forget to include other important elements such as reading, exercise, leisure and social commitments. This not only helps productivity but also promotes a balanced lifestyle. When I first gave away my day job, I documented my daily structure and divided the day into units of time to help me stay on track.

Eliminate Procrastination

Procrastination is the mother of time wasting! Identify any habits of yours which cause you to procrastinate or waste time, then eliminate them immediately. The most common time wasters are:

Social media

YouTube

Constantly checking e-mails

Text messaging

Chatting to friends during work time

Online shopping

Ensure you are not inventing things to do to avoid the important. This may sound strange, but it is a very common trap to fall into.

Go Faster

Make a conscious effort to move slightly faster with every action you take. This is the real fine tuning part of time management. Whether it’s walking to the letter box, typing an e-mail, sending a text message, cleaning the kitchen or taking a shower – everyone can usually squeeze a little bit extra out of their performance. By default, we are in relaxed

mode where every task is performed at a comfortable speed. I challenge you to spend a day where you push yourself to move just 10% faster than normal. This increase in productivity will deliver immediate results which will inspire you to continue pushing harder. Not only will you get more done, but you will be pumped up while you work which also makes relaxing and winding down at the end of the day so much sweeter. Besides the short term benefits of pushing yourself day to day, over a lifetime if you move just 10% faster in everything you do, you will create another 8 years of life!

Psychology

Making money in the markets is Simple. Buy with the trend with a good management. A complete amateur can open a trading account, place a trade, and out of sheer luck win big. This does not necessarily mean the individual is a talented trader. The real skill of trading lies in making consistent profits and allowing compound interest to do the work for you. The factor that determines your ability to make consistent profits is purely psychological. You could be an extremely intelligent person and be given the best trading strategies on the planet, yet be a terrible trader, not because you lack ability, but simply because you haven’t yet developed a trader’s mindset. You are about to learn exactly what that means, and more importantly how you can adopt this vital component right from the start of your trading career.

Mark Douglas, a world class trader and coach of 28 years, confirms that correct mindset is absolutely integral to a successful trading career.

“The defining characteristic that separates the consistent winners from everyone else is this: The winners have attained a mind-set—a unique set of attitudes—that allows them to remain disciplined, focused, and, above all, confident in spite of the adverse conditions. As a result, they are no longer susceptible to the common fears and trading errors that plague everyone else. Everyone who trades ends up learning something about the markets; very few people who trade ever learn the attitudes that are absolutely essential to becoming a consistent winner. Just as people can learn to perfect the proper technique for swinging a golf club or tennis racket, their consistency, or lack of it, will without a doubt come from their attitude. Traders who make it beyond “the threshold of consistency” usually experience a great deal of pain (both emotional and financial) before they acquire the attitude that allows them to function effectively in the market environment. The exceptions are usually those who were born into successful trading families or who started their trading careers under the guidance of someone who understood the true nature of trading, and, just as important, knew how to teach it. Why are emotional pain and financial disaster common among traders? The simple answer is that most of us weren’t fortunate enough to start our trading careers with the proper guidance.”

In my trading journey so far, I have lost count of the amount of traders I have met who have fallen short because they lack the correct mind-set for trading. Its actually one of my biggest bugs with teaching people. I love teaching traders, and I could spend all day doing it. However the one skill I can not teach is for traders is to adopt the right mind-set. Its something that can only be learnt by the individual. I generally do not think it can be taught either. In life we feel pain and losses more than growth and gains. Making money is short term happiness, but loosing month is long term pain and regret. For a Trader they have to experience that loss and pain of blowing an account, or loosing money to actually learn to change their habits in trading. Everyone is happy to trade without a stop loss, until they blow an account and feel the pain of loosing money. Unfortunately that is the only way to learn.

The Important of Rules

In order to become a consistently profitable trader, it is crucial that your behaviour is guided by a strict set of rules. There is no doubt that trading has inherent risks involved, therefore it is my aim to instil in you the importance of developing mental discipline. Throughout life, most situations we find ourselves in provide some kind of external structure where we have not had to create or rely on any form of internal guidelines. For example, when you play a game of sport and break a rule- there is an umpire there to monitor and call you out on your mistakes. In school, if you fail a test or show up late, there is a teacher present to monitor and reprimand you. Trading is the exact opposite- there are no external guidelines, no referee to call you out on your mistakes. When you approach the markets you harness the power of unlimited freedom to do whatever you want, therefore it is absolutely vital that you believe in, implement and always adhere to a set of internal guidelines that I will teach you throughout the course of these lessons.

Rule 1

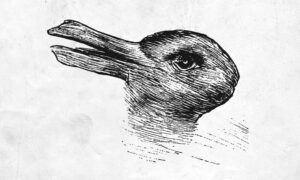

When most people are introduced to technical analysis they are not 100% comfortable with it. I believe that in a large majority of cases, this is due to how trading is depicted in movies such as ¨Wall Street¨. These movies imply that trading is a high risk/high reward game that requires 20 computer screens, a superior information feed and an in depth understanding of economics. Technical analysis, the way we teach, requires none of these elements. As I touched on in the introduction, technical analysis is purely identifying patterns in the market’s behaviour that represent an opportunity. As a method for predicting future price movements, this style of trading has proved far superior to a purely fundamental approach. The reason that more people are not successful in trading this way is that it relies heavily on your perception. For example, see the picture below.

If you’re like me you will be adamant that this is a picture of a rabbit. It was not until another trader pointed out that it could also be perceived as a duck, that I had to re-evaluate the way I was filtering the image I saw, to accommodate for this differing perception. Perception discrepancies present themselves frequently in trading, as Trader A may see a chart and perceive the information to be a possible reversal pattern, where as Trader B may perceive the complete opposite- despite looking at the exact same image! You may be

wondering what causes this. The simple answer- your brain! Specifically, your reticular formation: the part of the brain that is responsible for filtering incoming information.

Have you ever bought a new car and then started to notice the same model everywhere? As you probably know, it was not because everyone decided to go out and buy the same car that week. This is an example of how your reticular formation can highlight certain pieces of information that your brain receives through our five senses. On the other hand, it can just as easily discard certain pieces of information that the brain receives. If I was to have you count all of the white cars that you pass on a particular journey and report the number to me at the destination, this would be a fairly easy task. However, if I was then to ask you how many black cars you passed- it is extremely unlikely that you could answer accurately. Your brain had a specific job to count the number of white cars, so every time you passed a black car, the signal sent to the brain was filtered through your reticular formation and discarded as irrelevant information.

This is an example of how your reticular formation can completely blind you from something that is literally staring you in the face. This can present a huge problem for traders. Let’s say you notice the US dollar has steadily risen in price, and your gut instinct says that “it must be due for a turnaround”. Furthermore, the media paints a gloomy picture of the US economy, and “financial experts” all over the world predict a plummet in the US dollar, fuelling your gut feeling. This internal expectation that the US dollar is going to fall can act as a filter on your reticular formation and distort your perception of the chart. In this scenario let’s say one of your trend trading strategies signals an entry to buy the US dollar, even though you feel it will drop in price. An beginner trader will most likely approach the market in one of the following ways when presented with this situation:

1. Their mind will be so fixated on finding a selling opportunity, that the “buy” signal their strategy generated is filtered as irrelevant information and becomes invisible.

OR

2.They identify the “buy” signal, but have doubts about whether the trade will work, so they deliberately avoid placing the trade and justify their decision to themselves by saying “this is a different situation”, “the economy is in a bad state”, “the experts are saying it will drop” or something along those lines. Ironically, the worst thing that can happen in this circumstance is that their gut feeling is right, and the US dollar does drop. What this does is artificially inflates a trader’s confidence, reduces their respect for the strategy, and at a subconscious level associates a certain amount of pleasure with the act of breaking their rules, meaning they will do it again in the future.

Although the first approach can be attributed to an innocent mistake, the market is unforgiving and this kind of error will not only destroy the probability model of your strategy, but will likely result in inconsistent and poor results. The best way to identify and combat this habit is to back test your strategy weekly, and compare your trading results with the live market conditions. The second approach described above is far more sinister. When you begin consciously breaking your rules, you no longer have an edge in the market. Trading this way is the same as using your brokerage platform as an online casino (and will yield similar results). The lesson on probability will open your eyes to the concept of “trading an edge” and will illustrate the importance of applying a strategy with military grade accuracy and consistency.

One of your basic objectives as a trader is to perceive the opportunities that are available from a neutral perspective, rather than being threatened with the fear of loss. In order to

remain focused on these opportunities, you need to understand that the source of the threat is not the market- it is derived purely from your perception of it. The market displays information from a neutral perspective. It is not biased in any way, and, contrary to popular belief, it is not “against you”. The market should not be feared for it is merely providing you with an endless stream of opportunities to act on your own accord and make more money than you will ever need in a lifetime. If you ever find yourself operating from a state of fear, ask yourself: is the information something to be feared, or is it simply my perception of the information that is presenting it in this manner? This can be difficult to accept, so I will explain with an example. In this scenario, your last 5 trades lost. You identify an opportunity that is in line with your trading strategy. Instead of immediately executing the trade, you hesitate and start questioning whether it is “actually” a signal. This doubt compels you to start searching for information to support why this trade will lose. The information you gather is not normally something you would look for, and is certainly not incorporated in your strict trading strategy. In the time it has taken you to question yourself and find irrelevant evidence to support your doubt, the market has moved and is no longer conforming to your entry rules. The trade is winning at this point- you want to get in because the thought of missing out on profit is uncomfortable. This creates intense internal conflict. Paralysed by the conflict you take no action. You justify this to yourself by thinking “it was too risky”, yet feel regret as you watch the trade move in a winning direction. Those of you who have traded before have no doubt experienced this scenario. Ask yourself, were you perceiving the information from a neutral perspective or were your views biased, given you had lost 5 trades prior?

Let’s flip the situation around and say you were on a winning streak and subsequently felt very confident in your ability to anticipate the market’s moves. Do you think you would have viewed the information differently? Would you have still hesitated and gathered evidence to support the trade losing? Highly unlikely! In each of these scenarios the market generated identical information however, due to your state of mind, you perceived this information to have a different meaning.

So how do you ensure you are open to all information in a non-biased fashion? This can be answered with the first rule I was ever taught:

“Trade what you see, not what you think”

Those who have participated in any form of trading before may have personal experiences to draw from, in regards to how perception affects your ability to trade in a non-biased manner. I truly believe that my ability to trade successfully and consistently is derived in large part from learning the science of perception, which has allowed me to trade from a completely neutral state of mind. Understanding the dynamics of perception, which will allow you to “trade what you see, not what you think” will ensure you are in the right state of mind to take advantage of the lucrative opportunities the currency markets present to you.

A Story of two girls

To illustrate the importance of mindset, I want to present a brief story about two girls I read about.

The first girl is an African American child who was born into poverty to a single teenage mother. She experienced overwhelming hardship during her childhood, was raped at the age of nine by several family members and became pregnant at the age of fourteen. She had no stable home and was continually told she would go nowhere in life. The second girl was born into incredible wealth and fame. Her family was extremely successful in business, and had grand plans for her to carry on building the family empire. She attended the most prestigious schools, and was preened to take over a multimillion dollar empire.

Fast forward a few decades and who do you think is in a better situation? It’s easy to jump to a conclusion because generally a superior upbringing and better opportunities lead to a more comfortable and successful life, but without the right mindset, no amount of money, power, opportunity, or encouragement will ensure a positive outcome. The first girl had a dream, and she knew that despite her troubled childhood, she could rise above adversity and achieve it. She became an extremely successful businesswoman, actress, producer and philanthropist. At one point, she was ranked the richest African American of the 20th century and was the world’s only black billionaire. She has touched the lives of millions of people around the world and has been hailed the most influential woman on the planet. You may have heard of this girl, her name is Oprah Winfrey. On the other hand, the second girl was born with a silver spoon in her mouth and was presented with every opportunity from a young age. Although she could afford to flaunt her thousand dollar handbags and luxury cars, she spent little time, money and effort on improving her mindset and focussing on her “inner game”. Consequently, she grew up taking her family’s wealth for granted and her life began to spiral out of control. You may remember her from that sex tape in 2003, or her numerous legal breaches which found her in jail and sentenced to community service. Paris Hilton is an example of the modern phenomenon known as becoming a “celebutante”, the celebrity who rises to fame not because of their talent or work, but due to their inherited wealth and controversial lifestyle. In addition to her tarnished reputation, Hilton has had ongoing financial issues.

You may be wondering what these stories have to do with trading, but ask yourself, why did these two ladies end up with such vastly different lives? Oprah had all of the odds against her, whilst Paris Hilton had every opportunity for success, so why did one prosper and the other fail? It is important to understand that the common characteristic shared by every successful person in history is that they think differently from those who are not successful. Someone with a goal oriented and positive mindset has a distinct advantage over a person who lives day to day in the wishy-washy trance of routine. By having a clear, defined image of your ideal world firmly embedded into your brain, your mind will begin to focus on any opportunity in the external environment that will help you move towards that goal. On the other hand, if you have no target to aim for, no mission in life, and you are living as a slave to your habits, your mind will revert to basic human instinct which will force your primary focus to be on survival and reproduction.

Whether it is forex trading, property development, commodity investing or option writing, I can teach you the best money making strategies in the world, but if you are crippled with limiting beliefs, lack motivation, give up easily and do not maintain a mindset that is conducive to massive success, then these strategies will not work for you. Even if they do, you will likely squander most of your profits at some point, so that your level of prosperity returns to the level of your mindset. Our goal is not only to teach you profitable trading strategies, but to ensure you have the correct mental framework to become a professional trader. This includes thinking like a

trader, talking like a trader, walking like a trader, profiting like a trader, and believing in every fibre of your body that you are a successful currency trader.

In order to fully explain mindset and its influence on our lives, there are several related concepts which need to be defined and understood, the first of which is beliefs. We were not born with any of our beliefs; they were formed based on our experiences during certain situations. For example, as a child you may have had a dog as a family pet which was extremely loving and protective of you, and as a result you attached positive feelings towards dogs from this point onwards. Imagine however that your family owned an aggressive dog instead, which one day attacked you. This would have caused you to subconsciously link negative feelings towards dogs, that most likely would persist throughout your life. The process of attaching positive or negative feelings towards objects or situations based on our interaction with them begins the moment we are born, and continues until the day we die. Many of the beliefs that have the greatest impact on our lives were not gained by us consciously, but rather instilled by others before we were even old enough to make informed decisions regarding the information, or realise the negative implications of what we were being taught.

Beliefs and their impact on our lives

In the broadest sense, our beliefs shape the way we experience our lives. As our beliefs accumulate, we live our lives in a way that reflects what we have learned to believe. Consider how different your life would be if you had been born into a culture, religion, or political system that has very little, if anything, in common with the one you were born into. It might be hard to imagine, but what you would have learnt to believe about the nature of life and how the world works may not bear any resemblance to what you currently believe. Yet you would hold these other beliefs with the same degree of certainty as you do your current beliefs.

Let’s use an example about relationships. Our beliefs about relationships are usually a direct reflection of the quality of our past relationships, or the feelings we felt as a result of them. It is not uncommon to hear someone who has just come out of a painful break up say “I’m never getting into a relationship again!” This is not because all relationships are negative and hurtful, but because they have attributed feelings of pain towards the concept, and are naturally trying to avoid feeling this way again. Conversely, someone who has always been in great relationships is not likely to hold these same negative feelings. Someone with a negative view of relationships is likely to act differently when meeting someone new, in comparison to someone open to the concept of a new partner.

Beliefs in themselves cannot be right or wrong, as they are simply our own interpretations and perceptions of the world. What is important to realise though, is that our actions and decisions are all driven by the beliefs we have accumulated over time, some of which can be extremely empowering, and others very limiting. It is important to be able to identify the difference between these two, and eliminate any beliefs that are detrimental to your success both as a trader, and as a person.

Beliefs and their Impact on Trading

Although you may have never traded before, as long as you know what trading is, you will have formed some sort of belief about it. If you have traded before, this section is even more important, as you will have prior experiences fuelling your thoughts on the market. Regardless of your experience level, it is important to uncover any beliefs that could be harmful to your trading career and replace them with those that will ensure your success.

Investing vs trading

One of the most common misconceptions of currency trading is that it is just like investing in shares. Due to the huge media coverage and popularity of the share market, people who are new to trading often make the assumption that we “invest” in currencies based on their long term economic outlook, as in the share market. As we have noted several times previously, short term technical trading is very different from investing, and therefore should not be approached with an investment mindset. Here are some examples of how an investment mindset can negatively affect a technical trader:

Putting a trade on that is not part of your strategy because you “think the Australian Dollar

will go up, as the economy looks strong”.

Dollar cost averaging (buying more currency when a trade goes against you, as the fall in

price represents “good value” and it will lower your average purchase price).

Buy and hold (buying a currency and then waiting until you are old and grey before selling

it).

Risking more than 1% on a trade because you “know the US Dollar is weak and you will

make a lot of money going short”.

Failing to put a trade on where your strategy signals an entry, as it is in the opposite

direction of where you think that currency will go.

The above scenarios are all fuelled by investment type beliefs, where discretion and free thought are often used to make decisions. When technically trading currencies however, you must train yourself to think in probabilities and ensure you are trading with no emotion. If you have experience in the stock market you will need to retrain yourself to think like a short term technical trader, rather than a long term investor.

If you don’t believe in your system

In order for your system to work you must have 100% belief that it will return a positive result over time. Without full belief in your system, you are susceptible to making errors while trading, because what you believe subconsciously, will usually be revealed in reality. For example, let’s say you are having some dramas in your personal life and your friends suggest that a psychologist may be able to help you. You are sceptical, but decide to book an appointment simply to humour your friends. The psychologist will only be able to help you if you are open to their suggestions and fully believe they will help in solving your problems. An error that will frequently surface if you do not have belief in your trading system is when your strategy signals an entry, but your lack of belief renders you unable to perceive this as an entry, and therefore you avoid putting the trade on.

Financial Blueprint

Looking back over your life, have you always struggled to keep money, or do find it easy to attract large sums of cash into your life on a regular basis? What is it that allows some people to make more money than they will ever need in a lifetime, while others seem to blow every dollar they make? Is it because some people have better jobs, or that they have a higher income, or that they just get lucky? Of course not, otherwise there would be far more financially successful people in the world. During his professional boxing career, Mike Tyson made over $300 million US dollars, yet in 2003 he declared bankruptcy. If Tyson had invested his earnings at just 10% per annum he would have made $30 million a year in interest, yet somehow he managed to spend it all and ended up with nothing.

It is not enough just to be in the right place at the right time. T. Harv Eker, CEO of Peak Potentials Training, says that you actually have to be the right person, in the right place at the right time. Your character, your thinking and your beliefs around money are a critical part of what determines the level of your success. The vast majority of people simply do not have the internal capacity to create and hold on to large amounts of money. We have all heard of lottery winners who spend their fortunes in a very short period of time, only to end up in the same miserable situation that they were in before they won! Why does that happen? A person’s “financial blueprint” refers to their internal wealth thermostat. If your internal wealth thermostat is set to $10,000 it does not matter if you make $100,000 or $1,000,000 or $300,000,000 – your wealth will always fall to $10,000 to meet your thermostat. Lottery winners who have low financial thermostats will squander all of their new found wealth by giving family and friends hand outs and by purchasing too many unnecessary and unsustainable liabilities.

Your wealth with always rise or fall to meet your internal wealth thermostat.

T. Harv Eker’s book, “Secrets of the Millionaire Mind”, is a fantastic read for anyone wanting to change their financial blueprint. Below are the declarations Eker states you must make to yourself to achieve a mindset capable of handling money.

My inner world creates my outer world.

What I heard about money isn’t necessarily true. I choose to adopt new ways of thinking that

support my happiness and success.

I release my non supportive money experiences from the past and create a new and rich

future.

I observe my thoughts and entertain only those that empower me.

I create the exact level of my financial success!

My goal is to become a millionaire and more!

I commit to being rich.

I think big! I choose to help thousands and thousands of people!

I promote my value to others with passion and enthusiasm.

I am an excellent receiver. I am open and willing to receive massive amounts of money into

my life.

I choose to get paid based on my results.

I focus on building my net worth!

I am an excellent money manager.

My money works hard for me and makes me more and more money.

I am committed to constantly learning and growing.

T. Harv Eker has done extensive research into what creates successful people, and has found that most people are born with a threshold for money that is created not only by external influences, but also internal reinforcement. For example, if you were born into a family that struggled financially, it is likely that you would have picked up an attitude that money is hard to come by, and that you too would struggle financially throughout life. Conversely, if you were born into a family that has achieved financial success, it is likely that you would have a higher standard in regard to how much money you will attain throughout life. The good news is that you can change your money blueprint; you just need to be willing to make a conscious effort to do so!

Limiting Beliefs

In a previous example we talked about a psychologist who you might agree to see, only to please your friends. The limiting belief in your mind towards the psychologist in this situation would go something like this:

“Therapists can’t help me, I know people who have wasted a lot of money on therapy and nothing changed. I can deal with this myself.”

This is a generally held belief about therapists that will restrict your ability to benefit from their services. Limiting beliefs like this also exist in relation to money and trading, and actually limit your ability to be profitable in the markets. Everyone has unique opinions, however these are the most common limiting beliefs I have come across amongst new traders.

“I probably won’t make money but I’ll give it a try”

“Money can’t be that easy to make”

“I probably wouldn´t be able to trade full time”

“Money doesn’t grow on trees”

“What’s too good to be true usually is”

“Only institutions make money from trading, not ordinary people like me”

“I could lose everything if this doesn’t work out, it’s very risky”

“If I’m not good at this, it may not be for me”

I could spend all day refuting each of these statements, but the bottom line is this:

“What you focus on is what you will end up with”

If you don’t think you will make money- you won’t! If you don’t believe you will be good at trading- you won’t be! If you want to carry out an experiment of your own to test the power of limiting beliefs, go down to the bank and withdraw $100 in 5 dollar notes. If the experiment costs you $100, it is a cheap way to permanently remind you of the power of limiting beliefs. Take your money and set up a spot on a busy thoroughfare during peak hour and offer the passers-by a free 5 dollar note. You will be amazed to find out how many people see you, see the 5 dollar bill, yet still look away and continue walking. Many years ago a group of psychologists conducted this very experiment to see how people reacted when offered “free money”. Less than 5% of the people who walked by actually took up the offer. The psychologists concluded that a negative attitude, coupled with limiting beliefs towards money, the accumulation of money, and the concept of “easy money” were directly responsible for the amazing results.

Limiting beliefs can arise from statements, phrases and ideas that were ingrained deep into your subconscious from a young age. Beliefs such as:

“There is no such thing as a free lunch”

“To make money you need to work hard”

“Money just doesn’t come easily”

“I shouldn’t talk to strangers”

These phrases are frequently used by parents all over the world to caution their children, so it is no wonder that barely anyone will take your “free money”. The sad part of the experiment is that the 95% who missed out on the opportunity won’t even think of the scenario again. They will not realise that their limiting beliefs cost them the ability to make money, and therefore they will carry on throughout life holding onto these beliefs and pass them onto their children down the track. This is exactly the same principle I see in new traders every day. The money is right there, waving at them. However, 95% of traders won’t realize how easily they can take it if they just change their belief system and their mindset, so they keep on striving to get to work on time, and hold onto their limiting beliefs until their last breath.

Empowering Beliefs

The first step in replacing your limiting beliefs is to identify what is holding you back. In order to do this I recommend you have a list of goals, both in trading and in life (often you will find that limiting beliefs are not specific to one area of your life, but also affect your ability to perform in others). Goal setting will be discussed in detail in a later lesson on this subject. After this, look within yourself and identify any beliefs that are stopping you from achieving the goals in front of you. They may be similar to those I have listed above, or completely different. Regardless of what they are, it is important that you realise they must go!

Understand that your current circumstances in every aspect of life are directly governed by the beliefs that you have adopted and have employed throughout life up until this moment. The next step is to decide what to replace your limiting beliefs with. My lessons should provide you with a detailed understanding of the mindset that is necessary in trading, and I can provide you with an endless source of powerful information regarding other areas of your life that you may also wish to improve. Begin by modelling people who are already achieving the results you want. Reading books by authors who are successful in a certain field is the best way to duplicate their results for yourself. “Secrets of the Millionaire Mind” by T. Harv Eker, and “Think and Grow Rich” by Napoleon Hill are excellent books to start on, as they focus specifically on shifting beliefs.

Once you have identified a new belief, you have to install it. Essentially you need to immerse yourself in the new belief until your subconscious accepts it as true, and integrates it into your mental operating system. My favourite method is to use visualization, but some people swear by verbal affirmations, especially when combined with strong emotion.

Be patient with yourself because it can take a while for new beliefs to take hold. It usually takes me anywhere from a few weeks to several months before I’ve successfully integrated a new belief into my subconscious, depending on my internal resistance. If there’s no resistance, I can install a new belief in a day, but that is rare for significant changes. It takes time for my mind to accept the new belief as fact, instead of merely considering it as a possibility or an interesting idea, and it has to be successfully integrated with all the other thoughts going through my head. Installing a new belief is like getting an organ transplant. It takes a while for your body to accept the new organ, and there’s always a risk of rejection. You’ll know when your new belief has taken root, because you will begin to act in accordance with it without even thinking about it consciously. It will feel just like any other belief to you, in principle no different from a belief in gravity. You may find it difficult to shift your beliefs at first, but like any other skill, it takes practice. Don’t set yourself up for failure by trying to reprogram your whole life in one day. Don’t worry too much about straying from social norms. Whenever you want to push beyond average results, you’ll find yourself adopting uncommon beliefs. Wealthy people do not hold the same financial beliefs as the poor and middle class. Happy people do not have the same emotional beliefs as depressed people. And healthy people do not have the same diet and exercise beliefs as sickly or overweight people. The more exceptional you want your results to be, the more you have to push beyond the limitations of social conditioning. Exceptional results require exceptional beliefs.

Motivation

In order to succeed in trading, as with anything in life, you must be motivated to do so. It is all very well having the belief that you want to make extra money, but if you are not suitably motivated, it is unlikely that you will take action to achieve your goal. Due to the probability model in successful trading, remaining consistent in your trading routine is paramount, so it is essential that your motivation remains strong and consistent as well.

There are two ways to create motivation. The first is called “moving away” or “pain avoidance” motivation. This type of motivation is driven by a person’s need to avoid a bad circumstance that may cause them pain. An example of this could be an employee who is motivated to complete their work on time to avoid being fired, as this would cause financial pain. The employee is using the potentially unfavourable situation as motivation to move away from that circumstance. The other type is called “moving towards” or “pleasure seeking” motivation. An example of this behaviour is someone who is already fit and healthy who is training to run a marathon simply because it is their goal to do so. They are not driven by any type of pain, but rather a burning desire to achieve their goal. This person uses the feeling of happiness and fulfilment that they will receive after reaching their goal to create the motivation to complete the task at hand. Some people are motivated more by avoiding pain, and others by seeking pleasure, but it depends on the individuals personality and the intensity of their circumstances. However, I find that combining the two methods creates a drive more intense than any circumstance by itself. My motivation to quit work came from my absolute aversion for the 9-5 lifestyle combined with my passion to be financially free and able to do what I want, when I want. I found that by combining something that you strongly dislike and contrasting it with a situation that you desperately desire, you provide yourself with double the incentive!

“Passion comes from something you hate, something you love and the tension between the two.”

The main factor to consider when deciding upon what you will use as motivation, is that it needs to be something strong enough to serve its purpose every single day. One mistake people make is to use something that they believe should motivate them, such as “lots of money”. I had a good friend who asked me if I could teach him how to trade, because he knew it was a good opportunity to make money. However he never followed through with it because the motivation to “make money” obviously wasn’t a strong enough motivation for him. Believe it or not, money is a poor motivator. The freedom of being able to wake up with a blank canvas for the day and filling it with whatever your heart desires is a much more powerful motivator than simply “having more money”. Becoming a person who has learnt the skills required in order to sit down in front of a computer and make thousands of dollars profit in a short period of time, and then having the ability to teach friends and family how to replicate these results and become financially independent will motivate you more than the cash itself. It is best to spend some time and write down honestly what it is that trading can do for you. The obvious answer would be provide you with more income, but for some this may not be the most important factor- it could be spending more time with your family and less time at work. Make sure you focus on exactly why it is that you are becoming a trader, and keep it in your mind every day to fuel your success.

Persistence

Persistence is about creating a strong enough vision and reviewing it daily so that you are absolutely compelled to achieve your goals. If you cannot visualise yourself making money through trading, it is likely that you will not persist with it long enough to make any. I have no doubt that if it were not for my absolute commitment to becoming a successful trader; I would not be where I am today. A quote I heard early in my career that inspired me is:

“If you want to succeed as badly as you want to breathe, then you will be successful”

The meaning of this quote is simple- if you make goals and assign them the same importance as breathing; you will achieve them every time. Another example commonly used in relation to persistence is that of a baby learning to walk. If you had a child that was taking longer than usual to learn how to walk, would you simply give up? Of course not! Why? Because you are determined that it is necessary for that child to learn how to walk. There is never any doubt in your mind that they will succeed, you simply just keep trying until the child succeeds. An important factor that is present in this example is social proof. I’m sure you would agree there is a fair amount of social proof that people can walk, which makes persisting in this example rather easy. However, society does not dictate that you must become a successful trader. In fact, in some cases society dictates that you cannot become a successful trader. Therefore you must create confidence in your own mind and believe 100% that there is no excuse for not becoming a trading success.

Social Influence

This brings me to the impact of social influence. It is no secret that people who feel supported in their goals will achieve them far more easily than if they are surrounded by obstructive or unsupportive influences. For example, let’s say you grow up in a household where both of your parents are surgeons and they have high hopes for you to also become a doctor. They place you in the best school which specialises in scientific subjects, where your peers all have similar career aspirations. The problem is that you do not want to become a surgeon; you want to become a tattoo artist. Do you think that you would feel overly supported in your efforts to learn the art of tattooing? Probably not. Now let’s say you were born into a family that supported you in any venture that made you happy, and socialized with friends who had similar dreams. Chances are it would be far easier for you to become a professional tattoo artist in the second circumstance, as your supportive network helped you and fuelled your motivation to achieve your goals. Although surrounding yourself with supportive peers might sound like common sense, I believe it is a concept that is overlooked and ignored by many new traders.

Trading is not a social norm, and when people are presented with ideas that challenge their pre-programmed thoughts, they usually feel negatively towards them. For this reason, you should beware of the negative dream killers that you will face during your trading career. Remember that anyone who has not had the correct professional training in probability modelling, psychology, pattern recognition, strategy implementation and risk management is not in a position to be giving you advice, and if they feel compelled to do so, you should not listen to them. Unwelcome advice regarding trading of any nature is mostly negative, which stems from a bad personal experience and/or “tall poppy syndrome”. The sad truth is that most people do not want to see you do better than themselves, so if anyone attempts to limit you, pull you back, cut you down, instil fear within you or show negativity and sarcasm towards your goals, remember that they are simply jealous or threatened by your ambitions.

“Great spirits have always encountered violent opposition from mediocre minds. The mediocre mind is incapable of understanding the man who refuses to bow blindly to conventional prejudices and chooses instead to express his opinions courageously and honestly.” – Albert Einstein

Throughout my personal learning journey I have faced negative criticism every day. When I used to work my day job my boss told me that trading was far too risky, and even offered to help me find a suitable term deposit for my capital to earn a safe 6% per annum. I explained to him how I had made 5% for the week, but my energy was wasted, as he chuckled in disbelief. I soon learnt to “fly under the radar” and stopped sharing my progress with anyone who was negative or sarcastic towards my dreams. The day came when I was making more than my boss, and it was starting to cost me too much to go to work, so I happily handed in my resignation and became a full time trader. To my dismay, I have found that to this day it does not matter how many £10,000 weeks I have, or how many people watch me day trade the London open (and make more than the average employee makes for 40 hours of hard work), or the simple fact that I am now a full time trader – I am still plagued by negativity and disbelief when I discuss my profession amongst mediocre minds. If you are dedicated to becoming a trader, you must have a resilient character and be strong enough to put tall poppy cutters in their place. The negativity from some people will not end, even after you have proven yourself.

On the contrary, if you surround yourself with positive, successful people and traders alike, you will benefit in a number of ways. You will have people in your network that provide social proof that success in trading is attainable, which will motivate you to persist until you succeed. Also, when you are around people for long enough, you begin to model their behaviour, therefore it is much more beneficial to pick up positive habits and characteristics rather than those that could be detrimental to your success. A study was carried out a number of years ago which found that you can work out someone’s annual income within +/- 10% by finding out the annual income of their 5 closest friends and averaging them out. If you want to increase your income, make friends with people who earn more than you!

I encourage you to get around as many successful and supportive people as you can. If you just make one new friend who is successful, they will expose you to opportunities and ideas to which the average person would not have access. If you make 5 new successful friends, and eliminate any negative and unsupportive influences from your life, you will have no choice but to rise to the level of your environment and support network.

1.Have a clear, defined image of your ideal world firmly embedded into your brain, then

your mind will begin to focus on any opportunity in the external environment that will help

you move towards your goal.

2. You are not born with any beliefs, they are created based on your experiences, perceptions

and influences.

3. If you have experience in the stock market you will need to retrain yourself to think like a

short term technical trader, rather than a long term investor.

4. The beliefs you hold determine your behaviours and ultimately shape your life.

5. Beliefs can either limit you, or empower you in trading.

6. Your wealth with always rise or fall to meet your internal wealth thermostat.

7. There are two types of motivation, pain avoidance or pleasure seeking motivation. A

combination of both usually produces the best results.

8. In order to remain persistence, you must create a compelling reason as to why you must

succeed in trading.

9. What you focus on is what you will end up with.

10. Money is a poor motivator. The freedom of being able to wake up with a blank canvas for

the day and filling it with whatever your heart desires is a much more powerful motivator

than simply “having more money”.

11. If you want to succeed as badly as you want to breathe, then you will be successful.

12. Persist until you succeed.

13. Ensure you surround yourself with positive people and successful traders, as more often

than not you become a product of your own environment.

14. Take notice of everything you think and say and ensure it facilitates a peak mental state.

15. If you must watch the news, stay vigilant, alert and always ask questions. The mainstream

media is known to sacrifice the truth in exchange for a good story.

16. Beware of people with “tall poppy syndrome”. Remember most people do not want to see

you doing better than themselves.

17. Learn to master your thoughts, less your thoughts will master you.

18. Watch your mouth.

19. Remember to model confident and alert physiology

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Login

Accessing this course requires a login. Please enter your credentials below!